What you will find on this page: LATEST NEWS; Fossil fuel emissions have stalled; Analysis: Record surge of clean energy in 2024 halts China’s CO2 rise; does the world need hydrogen?; Mapped: global coal trade; Complexity of energy systems (maps); Mapped: Germany’s energy sources (interactive access); Power to the people (video); Unburnable Carbon (report); Stern Commission Review; Garnaut reports; live generation data; fossil fuel subsidies; divestment; how to run a divestment campaign guide; local council divestment guide; US coal plant retirement; oil conventional & unconventional; CSG battle in Australia (videos); CSG battle in Victoria; leasing maps for Victoria; coal projects Victoria

Huge task to decarbonise

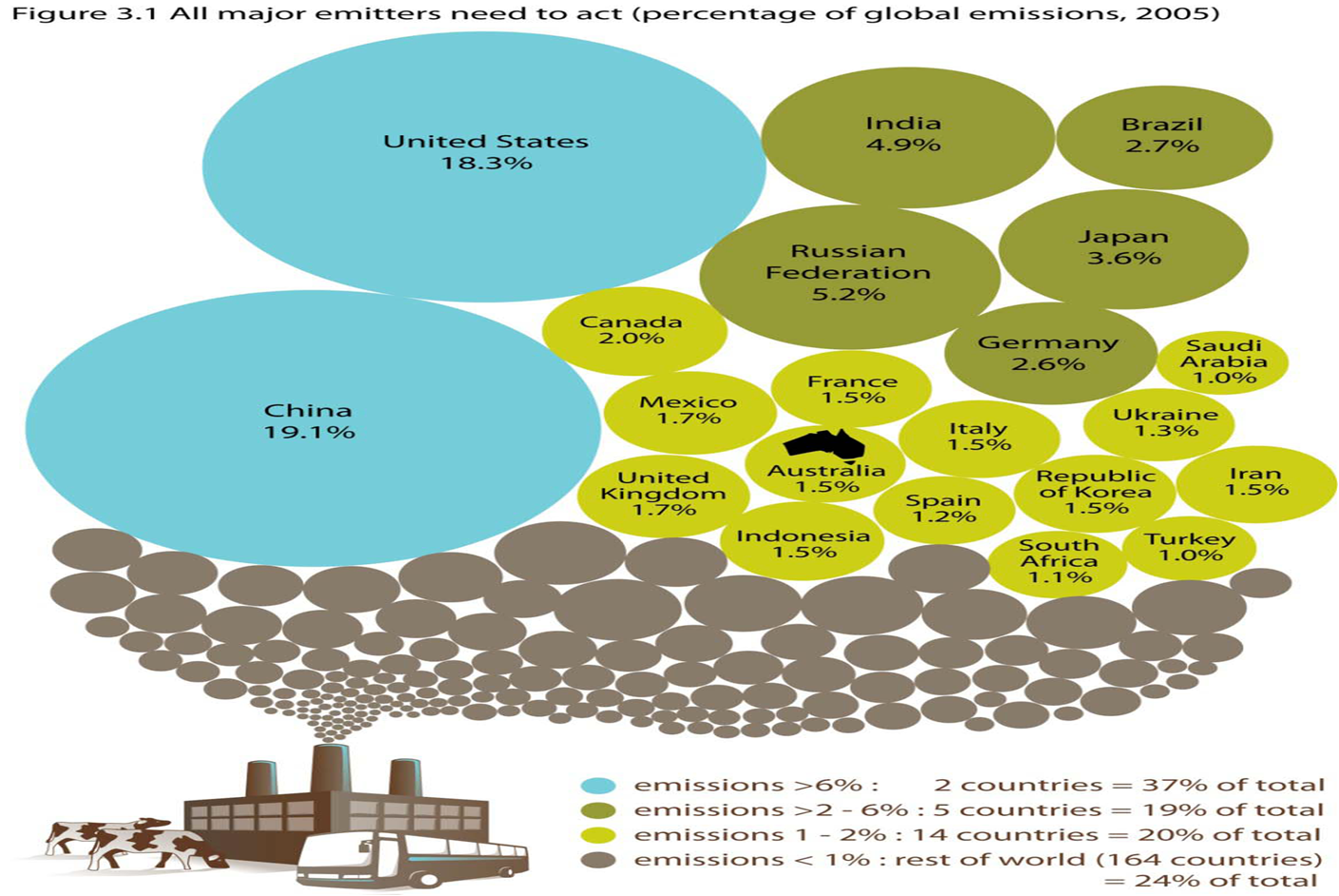

Source: Australian Delegation presentation to international forum held in Bonn in May 2012

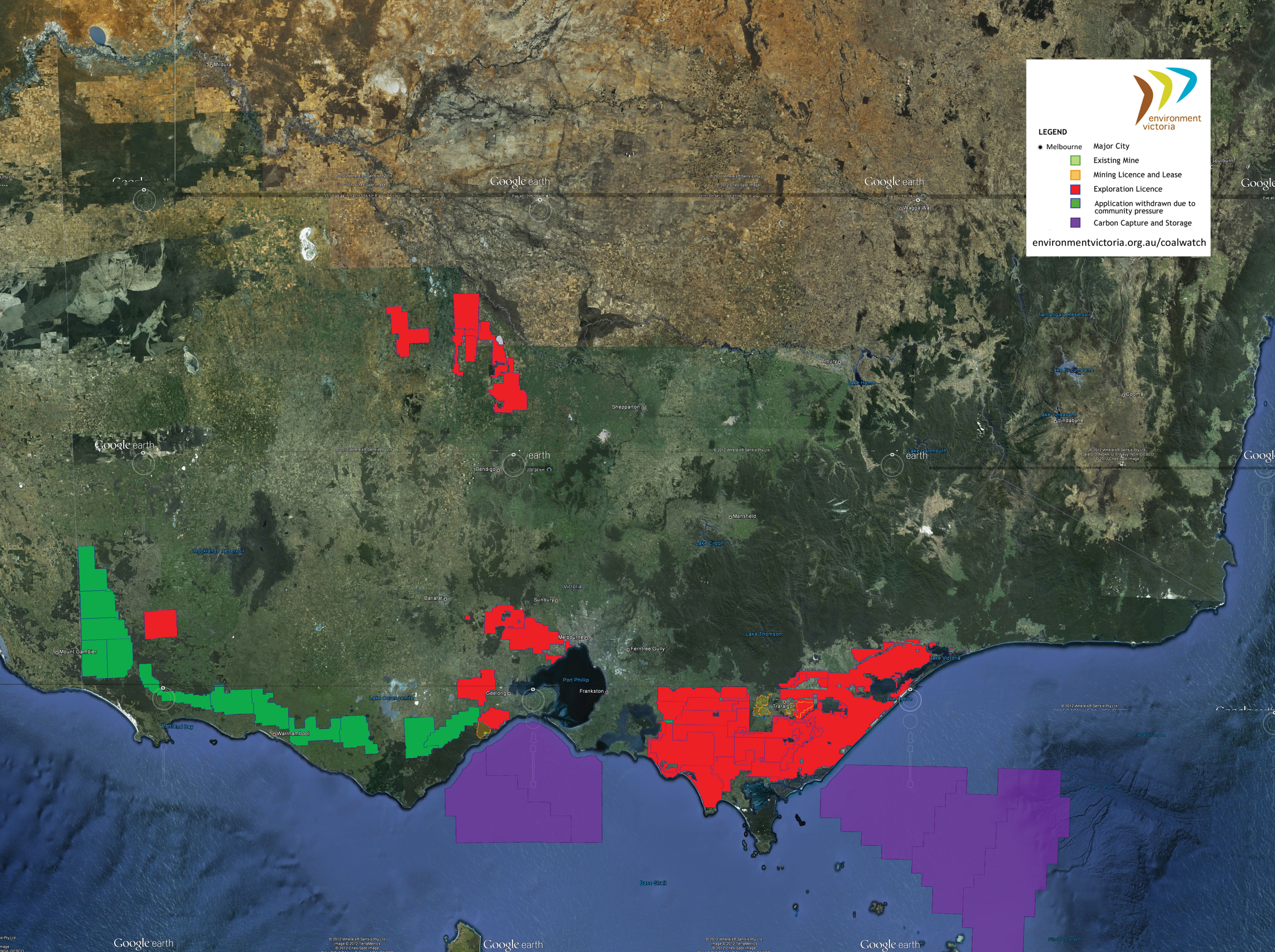

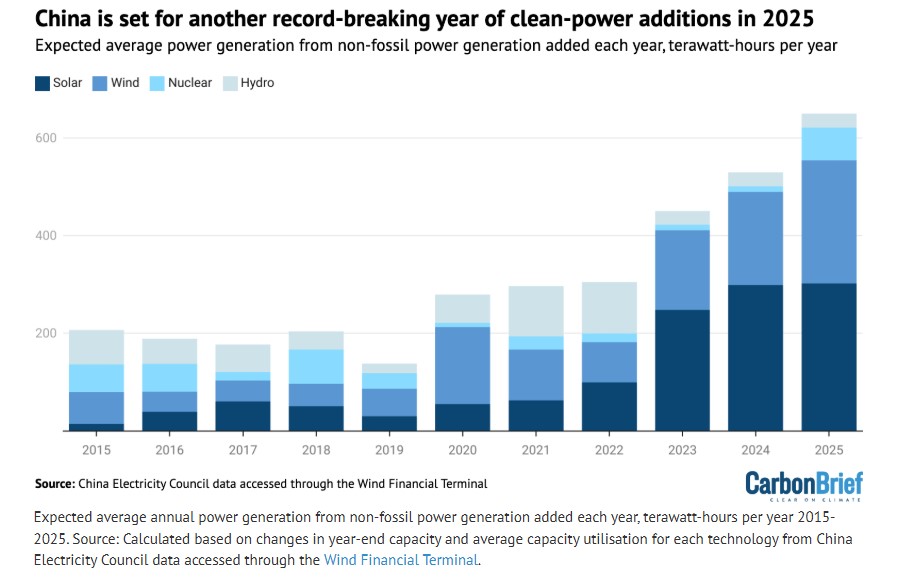

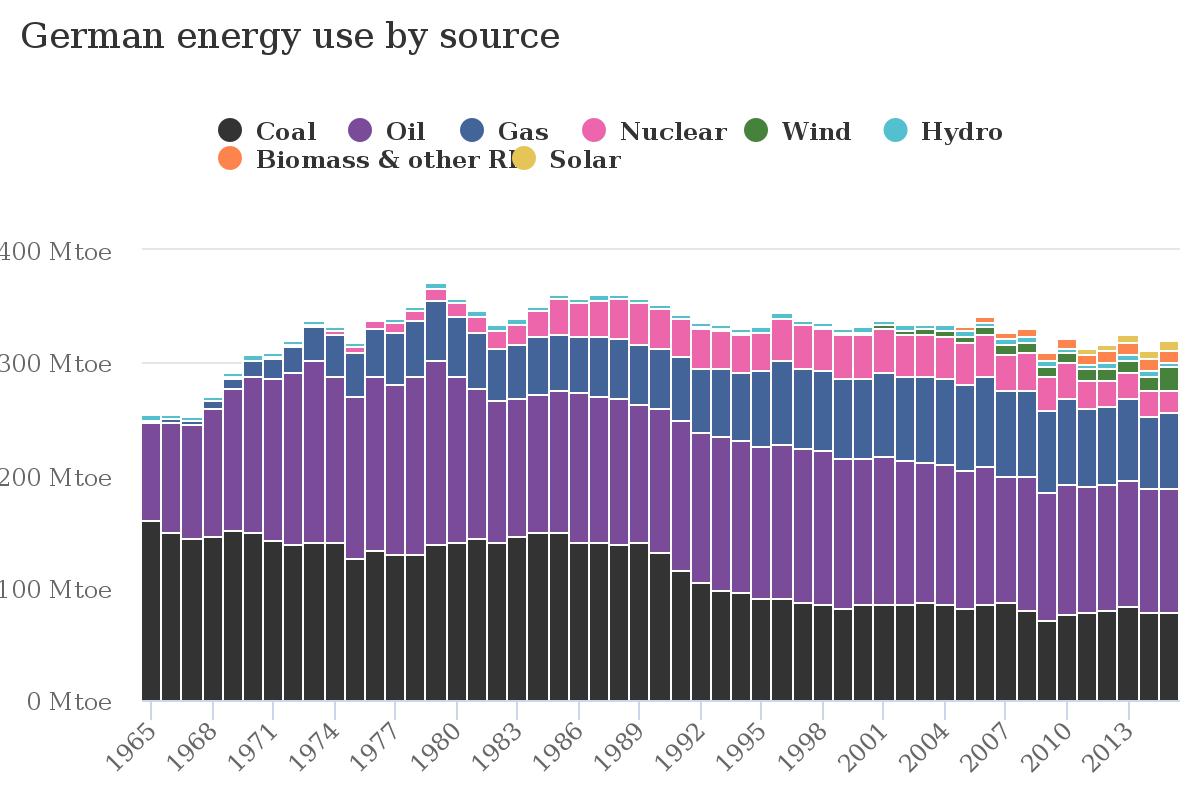

Latest News 12 February 2018, Renew Economy, S.A. to host Australia’s first green hydrogen power plant. The South Australia government has announced funding for what will be Australia’s first renewable-hydrogen electrolyser plant – a 15MW facility to be built near the end of the grid at Port Lincoln on the Eyre Peninsula. The “green hydrogen” plant – to be built by Hydrogen Utility (H2U), working with Germany’s thyssenkrupp – will include a 10MW hydrogen-fired gas turbine, fuelled by local wind and solar power, and a 5MW hydrogen fuel cell. Both will supply power to the grid, will support two new solar farms and a local micro-grid, and will also include “distributed ammonia” that can be used as an industrial fertiliser for farmers and aquaculture operators. The $117.5 million project, which will receive a $4.7 million grant and a $7.5 million loan from South Australia’s Renewable Technology Fund, is being described as a “globally-significant demonstrator project” for the emerging hydrogen energy sector. Read More here 12 February 2018, Climate News Network, Hydrogen could see off fossil fuels. Hydrogen is the least talked-about renewable energy but has the greatest potential to replace fossil fuels, both to heat homes and to provide fuel for road transport. The possibility of using hydrogen has been known about for generations, but only in the last two years has it become both practical and financially viable to see it as a large-scale competitor to both gas and oil. Networks of hydrogen filling stations are now being opened in Europe and parts of the US. Batteries for road transport have attracted most of the recent publicity around renewables and have become the focus of many governments with targets for switching away from petrol and diesel, particularly in cities with air pollution problems. But hydrogen has even greater potential because its only emissions are pure water and warm air. Storage potential What has made hydrogen so attractive is that it can use surplus renewable electricity from wind and solar farms by using electrolysers to produce hydrogen. This is a process of passing an electric current through water and converting it into oxygen and hydrogen. The hydrogen can then be stored. Read More here 15 January 2018, Climate News Network, District heating warms cities without fossil fuels. Heating homes and offices without adding to the dangers of climate change is a major challenge for many cities, but re-imagined district heating is now offering an answer. A district heating scheme is a network of insulated pipes used to deliver heat, in the form of hot water or steam, from where it is generated to wherever it is to be used. As a way of providing warmth for thousands of homes, typically in multi-storey apartment buildings, district heating has a long history in eastern Europe and Russia. But the hot water it distributes typically comes from power stations burning coal or gas, which means more greenhouse gas emissions. Tapping into other forms of producing hot water, from renewable energy, bio-gas or capturing waste heat from industrial production, supermarkets or IT systems, provides alternative sources of large scale heating without adding to the carbon dioxide in the atmosphere. Sweden has pioneered the switch from fossil fuels to other ways of heating water. The Swedish Environmental Protection Agency says the country has gone from almost exclusively relying on fossil fuels to being 90% powered by renewable and recycled heat in 2017. Read More here 11 January 2018, The Conversation, A month in, Tesla’s SA battery is surpassing expectations. It’s just over one month since the Hornsdale power reserve was officially opened in South Australia. The excitement surrounding the project has generated acres of media interest, both locally and abroad. The aspect that has generated the most interest is the battery’s rapid response time in smoothing out several major energy outages that have occurred since it was installed. Following the early success of the SA model, Victoria has also secured an agreement to get its own Tesla battery built near the town of Stawell. Victoria’s government will be tracking the Hornsdale battery’s early performance with interest. Generation and Consumption Over the full month of December, the Hornsdale power reserve generated 2.42 gigawatt-hours of energy, and consumed 3.06GWh. Since there are losses associated with energy storage, it is a net consumer of energy. This is often described in terms of “round trip efficiency”, a measure of the energy out to the energy in. In this case, the round trip efficiency appears to be roughly 80%. The figure below shows the input and output from the battery over the month. As can be seen, on several occasions the battery has generated as much as 100MW of power, and consumed 70MW of power. The regular operation of battery moves between generating 30MW and consuming 30MW of power. Read More here 29 November 2023, RealClimate: Science denial is still an issue ahead of COP28. It is 33 years now since the IPCC in its first report in 1990 concluded that it is “certain” that greenhouse gas emissions from human activities “will enhance the greenhouse effect, resulting on average in an additional warming of the Earth’s surface.” That has indeed happened as predicted, it has been confirmed by a zillion studies and has been scientific consensus for decades. Yet, when the next global climate summit is coming up (it’s starting tomorrow), we don’t only learn that the host, United Arab Emirates, intends to use the event for new oil deals. We also see more attempts to cast doubt that global warming is caused by emissions from burning oil, gas and coal – as so often before these summits. This time making the rounds is a “discussion paper” published by Statistics Norway. It is noteworthy not because it contains anything new (it doesn’t), but because despite clearly violating the established standards of good scientific practice, it was published by a government agency. That’s why it is having an impact in non-scientific quarters including the corporate world, and it has even been cited in a submission to proceedings of the German parliament. The flood of fallacies or deceptions begins with the paper’s title: “To what extent are temperature levels changing due to greenhouse gas emissions?” But the effect of greenhouse gases is not even investigated in the paper – which suggests the title is politically motivated. And the paper revolves around ignoring past studies and basic physics, using dubious sources, and the glaring blunder of arguing that warming at any individual weather station might be caused by random weather variations, without ever wondering how it is possible that these supposed random variations go in the same direction all over the planet: in the direction of warming. The paper provides a good opportunity to illustrate how climate science obfuscation works, and to remind readers how we actually know for sure that greenhouse gas emissions are indeed responsible for modern global warming. Read more here 24 November 2023, Climate Home News: The ‘inevitable’ fossil fuel fight set to dominate Cop28. Could petrostate UAE be the climate summit host that lands an international agreement to exit coal, oil and gas? Phasing down fossil fuels is “inevitable” and “essential”. It is hard to imagine the CEO of an oil major saying that 10 years, five years, even one year ago. It’s a measure of how far the discourse has moved since the Paris Agreement that Sultan Al Jaber has taken that line in the run-up to Cop28. As president of the UN climate summit starting in Dubai on 30 November, Al Jaber could not ignore mounting calls to quit coal, oil and gas. “We cannot address climate catastrophe without addressing its root cause: fossil fuel dependence,” said UN chief Antonio Guterres last week. “Cop28 must send a clear signal that the fossil fuel age is out of gas – that its end is inevitable.” But Al Jaber has not quit the day job as chief of Emirati state-owned oil company Adnoc, which is increasing production. The conflict of interest is writ large. And despite the longstanding scientific consensus that burning fossil fuels is the main driver of the climate crisis, there was no political consensus to name them in UN climate decisions until very recently. At the 2021 climate summit in Glasgow, UK, countries made a breakthrough agreement to phase down coal power generation. A group of around 80 countries pushed to extend that to oil and gas in Sharm-el-Sheik last year, but were stonewalled. Will Al Jaber’s rhetoric translate into an international agreement? Phasing down or cashing in? The science is clear: we need to substantially reduce the use of fossil fuels to stand a realistic chance of limiting global warming to 1.5C, the Intergovernmental Panel on Climate Change said. There is no room for new oil and gas fields, the International Energy Agency agreed. While there is money to be made, though, mining and drilling continue. Buoyant oil prices since Russia invaded Ukraine last year have spurred development. The top 20 fossil fuel-producing nations plan to extract twice as much by 2030 as the level consistent with meeting the Paris Agreement goals, according to the UN’s 2023 Production Gap report. Read more here 20 October 2023, Climate Home News: World Bank controversy sends loss and damage talks into overtime. Developing countries are outraged by a proposal to host a climate loss and damage fund at the World Bank, painting it as a US power grab. The president of the next UN climate summit, Cop28, has told government negotiators they must agree how to set up a new loss and damage fund before leaving the Egyptian city of Aswan. The United Arab Emirates’ Sultan Al Jaber addressed the 24 members of the transitional committee by video link on Friday morning, the last official day of talks. At Cop27 in Sharm el-Sheikh, governments tasked the committee with working out what a new loss and damage fund for climate victims should look like and present their proposals to Cop28 in November. The fund is supposed to channel money to people who have suffered loss and damage caused by climate change. This could mean rebuilding homes after a hurricane or supporting farmers displaced by recurrent drought. Failure to reach consensus risks delaying support to those in need. But developing countries were incensed by a proposal to host the fund at the World Bank, painting it as a US power grab. And rich-poor divides persisted on how to define the “vulnerable” groups eligible for funds and who gets to control spending. Al Jaber accused the negotiators of dragging their feet and told them not to leave this task to ministers. “I expect you to deliver,” he said. “If I don’t see real and tangible results, that will not be acceptable.” Read more here 7 September 2023, Climate Home News: A wolf in sheep’s clothing: why Africa should shun carbon markets. Turning Africa into a source of carbon credits will benefit polluters and middlemen, not most Africans and not the planet. There is increasing hype and push for so-called voluntary carbon markets in Africa. Politicians, businesses, some NGOs and big philanthropy are trying to get an African Carbon Market Initiative off the ground, which would allow companies to buy carbon credits in exchange for continued emissions. It’s become a major topic of controversy in the run up to the Africa Climate Summit this month. But Africa’s leaders should think twice before supporting this wolf in sheep’s clothing. The idea is that some of the money paid by the corporations for these “carbon credits” – or more accurately, permits to pollute – would go towards projects in Africa that avoid or reduce emissions: renewable energy projects, or land and nature schemes that aim to capture carbon from the atmosphere. But a number of key questions are being ignored – do they work for African people, the climate and development? or western polluters, they are a silver bullet painkiller that allows them to keep pumping greenhouse gases into the atmosphere. But for Africa, they are a placebo drug that ends up making the pain of climate change far worse. Africa is indeed right to demand climate funding from the global north, who caused the climate crisis which is devastating African people, economies, and nature in the first place. But instead of signing up to a carbon market initiative that is full of booby traps, African leaders should use the opportunity to work together with others in the global south to interrogate where the real and essential money is for the critical role we play in protecting forests and nature, without which the Paris Agreement would fail? Where is the money for the actions to reduce emissions and adapt to climate change that we need and deserve? Read more here 21 July 2025, RealClimate: National Climate Assessment links. For some reason, it has become hard to locate the various National Climate Assessments (NCAs) that have been produced by the USGCRP over the decades (and it’s pretty hard to find the USGRCP as well…). However, the reports are still accessible if you know where to look. So for future reference, here are all the links (and we’ve downloaded the pdfs locally so that they will always be available here). Read more here 17 July 2025, AllSides: 20 States Sue Trump Admin Over Termination of FEMA’s BRIC Program. A coalition of 20 states has filed a lawsuit against the Trump administration over its decision to terminate FEMA’s Building Resilient Infrastructure and Communities (BRIC) program, a grant program aimed at protecting communities from natural disasters. The Details: The lawsuit alleges that FEMA unlawfully terminated the BRIC program without congressional approval. It claims the termination puts lives at risk by making it harder for communities to protect themselves against future extreme weather events. The states involved in the lawsuit are Arizona, California, Colorado, Connecticut, Delaware, Illinois, Maine, Maryland, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Carolina, Oregon, Pennsylvania, Rhode Island, Vermont, Washington, and Wisconsin. For Context: The BRIC program, established in 2018, replaced a similar FEMA initiative known as the Pre-Disaster Mitigation program. It has funded nearly 2,000 projects with approximately $4.5 billion, saving taxpayers more than $150 billion that would have been spent on rebuilding property damaged or destroyed by disasters. FEMA announced the termination of the BRIC program in April as part of efforts to eliminate “waste, fraud, and abuse.” Read more here 15 July 2025, AP News: Trump administration says it won’t publish major climate change reports on NASA website as promised. The Trump administration on Monday took another step to make it harder to find major, legally mandated scientific assessments of how climate change is endangering the nation and its people. Earlier this month, the official government websites that hosted the authoritative, peer-reviewed national climate assessments went dark. Such sites tell state and local governments and the public what to expect in their backyards from a warming world and how best to adapt to it. At the time, the White House said NASA would house the reports to comply with a 1990 law that requires the reports, which the space agency said it planned to do. But on Monday, NASA announced that it aborted those plans. On July 3, NASA put out a statement that said, “All preexisting reports will be hosted on the NASA website, ensuring continuity of reporting.” “This document was written for the American people, paid for by the taxpayers, and it contains vital information we need to keep ourselves safe in a changing climate, as the disasters that continue to mount demonstrate so tragically and clearly,” said Texas Tech climate scientist Katharine Hayhoe. She is chief scientist at The Nature Conservancy and co-author of several past national climate assessments. Copies of past reports are still squirreled away in the National Oceanic and Atmospheric Administration’s library and the latest report and its interactive atlas can be seen here. Read more here 15 July 2025, The Conversation: Federal Court rules Australian government doesn’t have a duty of care to protect Torres Strait Islanders from climate change. The Federal Court has handed down its long-awaited judgement in a four-year climate case brought by Torres Strait Islanders. Elders Uncle Pabai Pabai and Uncle Paul Kabai took the Australian government to court on behalf of their community, arguing the government has a duty of care to protect them from climate change. They also asked the court to legally recognise the cultural loss and harm they are experiencing from sea-level rise and climate-induced flooding. But the court declined to recognise either duty or to legally recognise cultural harm. Many climate justice advocates hoped today’s decision would be the climate equivalent of the famous Mabo decision, which recognised native title. There are many parallels. At stake was the legal recognition of the harms and loss of connection to Country that Australia’s First Peoples are experiencing through government inaction on climate change…What the Federal Court said Justice Michael Wigney’s judgement emphasised the existential threat of climate change. It noted Torres Strait Islanders are particularly vulnerable to climate impacts and face a “bleak future” unless urgent action is taken. But it accepted the government’s argument that setting emissions reductions targets, and allocating funding for protective infrastructure, involves “policy” considerations a court can’t review. Read more here 27 January 2025, Carbon Brief: A record surge of clean energy kept China’s carbon dioxide (CO2) emissions below the previous year’s levels in the last 10 months of 2024. However, the new analysis for Carbon Brief, based on official figures and commercial data, shows the tail end of China’s rebound from zero-Covid in January and February, combined with abnormally high growth in energy demand, stopped CO2 emissions falling in 2024 overall. While China’s CO2 output in 2024 grew by an estimated 0.8% year-on-year, emissions were lower than in the 12 months to February 2024. Other key findings of the analysis include: As ever, the latest analysis shows that policy decisions made in 2025 will strongly affect China’s emissions trajectory in the coming years. In particular, both China’s new commitments under the Paris Agreement and the country’s next five-year plan are being prepared in 2025. Read More Here 3 November 2020, Carbon Brief: Hydrogen gas has long been recognised as an alternative to fossil fuels and a potentially valuable tool for tackling climate change. Now, as nations come forward with net-zero strategies to align with their international climate targets, hydrogen has once again risen up the agenda from Australia and the UK through to Germany and Japan. In the most optimistic outlooks, hydrogen could soon power trucks, planes and ships. It could heat homes, balance electricity grids and help heavy industry to make everything from steel to cement. But doing all these things with hydrogen would require staggering quantities of the fuel, which is only as clean as the methods used to produce it. Moreover, for every potentially transformative application of hydrogen, there are unique challenges that must be overcome. In this in-depth Q&A – which includes a range of infographics, maps and interactive charts, as well as the views of dozens of experts – Carbon Brief examines the big questions around the “hydrogen economy” and looks at the extent to which it could help the world avoid dangerous climate change. Access full article here Fossil fuel emissions have stalled 14 November 2016, The Conversation, Fossil fuel emissions have stalled: Global Carbon Budget 2016. For the third year in a row, global carbon dioxide emissions from fossil fuels and industry have barely grown, while the global economy has continued to grow strongly. This level of decoupling of carbon emissions from global economic growth is unprecedented.Global CO₂ emissions from the combustion of fossil fuels and industry (including cement production) were 36.3 billion tonnes in 2015, the same as in 2014, and are projected to rise by only 0.2% in 2016 to reach 36.4 billion tonnes. This is a remarkable departure from emissions growth rates of 2.3% for the previous decade, and more than 3% during the 2000’s. Read More here Do you want to understand the complexity of energy systems which support our high consumption lifestyles? Most people don’t give too much thought to where their electricity comes from. Flip a switch, and the lights go on. That’s all. The origins of that energy, or how it actually got into our homes, is generally hidden from view. This link will take you to 11 maps which explain energy in America (it is typical enough as an example of a similar lifestyle as Australia – when I find maps for Oz I’ll add them in) e.g. above map showing the coal plants in the US. Source: Vox Explainers Mapped: how Germany generates its electricity – another example Power to the People – Lock the Gate looks back at the wins of 2015 And there’s lots more coming up in 2016. Some of the big priorities coming up next for the “Lock the Gate” movement are: If you want to give “Lock the Gate” your support – go here for more info This new report reveals that the pollution from Australia’s coal resources, particularly the enormous Galilee coal basin, could take us two-thirds of the way to a two degree rise in global temperature. To Read More and download report The 2006 UK government commissioned Stern Commission Review on the Economics of Climate Change is still the best complete appraisal of global climate change economics. The review broke new ground on climate change assessment in a number of ways. It made headlines by concluding that avoiding global climate change catastrophe was almost beyond our grasp. It also found that the costs of ignoring global climate change could be as great as the Great Depression and the two World Wars combined. The review was (still is) in fact a very good assessment of global climate change, which inferred in 2006 that the situation was a global emergency. Read More here The Garnaut Climate Change Review was commissioned by the Commonwealth, state and territory governments in 2007 to conduct an independent study of the impacts of climate change on the Australian economy. Prof. Garnaut presented The Garnaut Climate Change Review: Final Report to the Australian Prime Minister, Premiers and Chief Ministers in September 2008 in which he examined how Australia was likely to be affected by climate change, and suggested policy responses. In November 2010, he was commissioned by the Australian Government to provide an update to the 2008 Review. In particular, he was asked to examine whether significant changes had occurred that would affect the analysis and recommendations from 2008. The final report was presented May 2011. Since then the Professor has regularly participated in the debate of fossil fuel reduction, as per his latest below: To access his reports; interviews; submissions go here 27 May 2015, Renew Economy, Garnaut: Cost of stranded assets already bigger than cost of climate action. This is one carbon budget that Australia has already blown. Economist and climate change advisor Professor Ross Garnaut has delivered a withering critique of Australia’s economic policies and investment patterns, saying the cost of misguided over-investment in the recent mining boom would likely outweigh the cost of climate action over the next few decades. Read More here Live generation of electricity by fuel type Fossil Fuel Subsidies – The Age of entitlement continues 24 June 2014, Renew Economy, Age of entitlement has not ended for fossil fuels: A new report from The Australia Institute exposes the massive scale of state government assistance, totalling $17.6 billion over a six-year period, not including significant Federal government support and subsidies. Queensland taxpayers are providing the greatest assistance by far with a total of $9.5 billion, followed by Western Australia at $6.2 billion. The table shows almost $18 billion dollars has been spent over the past 6 years by state governments, supporting some of Australia’s biggest, most profitable industries, which are sending most of the profits offshore. That’s $18 billion dollars that could have gone to vital public services such as hospitals, schools and emergency services. State governments are usually associated with the provision of essential services like health and education so it will shock taxpayers to learn of the massive scale of government handouts to the minerals and fossil fuel industries. This report shows that Australian taxpayers have been misled about the costs and benefits of this industry, which we can now see are grossly disproportionate. Each state provides millions of dollars’ worth of assistance to the mining industry every year, with the big mining states of Queensland and Western Australia routinely spending over one billion dollars in assistance annually. Read More here – access full report here What is fossil fuel divestment? Local Governments ready to divest Aligning Council Money With Council Values A Guide To Ensuring Council Money Isn’t Funding Climate Change. 350.org Australia – with the help of the incredible team at Earth Hour – has pulled together a simple 3-step guide for local governments interested in divestment. The movement to align council money with council values is constantly growing in Australia. It complements the existing work that councils are doing to shape a safe climate future. It can also help to reshape the funding practices of Australia’s fossil fuel funding banks. The steps are simple. The impact is huge.The guide can also be used by local groups who are interested in supporting their local government to divest as a step-by-step reference point. Access guide here How coal is staying in the ground in the US Sierra Club Beyond Coal Campaign May 2015, Politico, Michael Grunwald: The war on coal is not just political rhetoric, or a paranoid fantasy concocted by rapacious polluters. It’s real and it’s relentless. Over the past five years, it has killed a coal-fired power plant every 10 days. It has quietly transformed the U.S. electric grid and the global climate debate. The industry and its supporters use “war on coal” as shorthand for a ferocious assault by a hostile White House, but the real war on coal is not primarily an Obama war, or even a Washington war. It’s a guerrilla war. The front lines are not at the Environmental Protection Agency or the Supreme Court. If you want to see how the fossil fuel that once powered most of the country is being battered by enemy forces, you have to watch state and local hearings where utility commissions and other obscure governing bodies debate individual coal plants. You probably won’t find much drama. You’ll definitely find lawyers from the Sierra Club’s Beyond Coal campaign, the boots on the ground in the war on coal. Read More here Oil – conventional & unconventional May 2015, Oil change International Report: On the Edge: 1.6 Million Barrels per Day of Proposed Tar Sands Oil on Life Support. The Canadian tar sands is among the most carbon-intensive, highest-cost sources of oil in the world. Even prior to the precipitous drop in global oil prices late last year, three major projects were cancelled in the sector with companies unable to chart a profitable path forward. Since the collapse in global oil prices, the sector has been under pressure to make further cuts, leading to substantial budget cuts, job losses, and a much more bearish outlook on expansion projections in the coming years. Read full report here. For summary of report USA Sierra Club Beyond Oil Campaign Coal Seam Gas battle in Australia Lock the Gate Alliance is a national coalition of people from across Australia, including farmers, traditional custodians, conservationists and urban residents, who are uniting to protect our common heritage – our land, water and communities – from unsafe or inappropriate mining for coal seam gas and other fossil fuels. Read more about the missions and principles of Lock the Gate. Access more Lock the Gate videos here. Access Lock the Gate fact sheets here 2014: Parliament of Victoria Research Paper: Unconventional Gas: Coal Seam Gas, Shale Gas and Tight Gas: This Research Paper provides an introduction and overview of issues relevant to the development of unconventional gas – coal seam, shale and tight gas – in the Australian and specifically Victorian context. At present, the Victorian unconventional gas industry is at a very early stage. It is not yet known whether there is any coal seam gas or shale gas in Victoria and, if there is, whether it would be economically viable to extract it. A moratorium on fracking has been in place in Victoria since August 2012 while more information is gathered on potential environmental risks posed by the industry. The parts of Victoria with the highest potential for unconventional gas are the Gippsland and Otway basins. Notably, tight gas has been located near Seaspray in Gippsland but is not yet being produced. There is a high level of community concern in regard to the potential impact an unconventional gas industry could have on agriculture in the Gippsland and Otway regions. Industry proponents, however, assert that conventional gas resources are declining and Victoria’s unconventional gas resources need to be ascertained and developed. Read More here 28 January 2015, ABC News, Coal seam gas exploration: Victoria’s fracking ban to remain as Parliament probes regulations: A ban on coal seam gas (CSG) exploration will stay in place in Victoria until a parliamentary inquiry hands down its findings, the State Government has promised. There is a moratorium on the controversial mining technique, known as fracking, until the middle of 2015. The Napthine government conducted a review into CSG, headed by former Howard government minister Peter Reith, which recommended regulations around fracking be relaxed. Labor was critical of the review, claiming it failed to consult with farmers, environmental scientists and local communities. Read more here Keep up to date and how you can be involved here Friends of the Earth Melbourne Coal & Gas Free Victoria 20 May 2015, FoE, Inquiry into Unconventional Gas: Check here for details on the Victorian government’s Inquiry into unconventional gas. The public hearings have not yet started, however the Terms of Reference have been released. The state government’s promised Inquiry into Unconventional Gas has now been formally announced, with broad terms of reference (TOR). FoE’s response to the TOR is available here. The Upper House Environment and Planning Committee will manage the Inquiry. You can find the Inquiry website here. The final TOR will be determined by the committee. Significantly, it is a cross party committee. The Chair is a Liberal (David Davis), and there is one National (Melinda Bath), one Green (Samantha Dunn), three from the ALP (Gayle Tierney, Harriet Shing, Shaun Leane), an additional MP from the Liberals (Richard Dalla-Riva), and one MP from the Shooters Party (Daniel Young). Work started by the previous government, into water tables and the community consultation process run by the Primary Agency, will be released as part of the inquiry.The moratorium on unconventional gas exploration will stay in place until the inquiry delivers its findings. The interim report is due in September and the final report by December. There is the possibility that the committee will amend this timeline if they are overwhelmed with submissions or information. Parliament will then need to consider the recommendations of the committee and make a final decision about how to proceed. This is likely to happen when parliament resumes after the summer break, in early 2016. Quit Coal is a Melbourne-based collective that campaigns against the expansion of the coal and unconventional gas industries in Victoria. Quit Coal uses a range of tactics to tackle this problem. We advise the broader Victorian community about plans for new coal and unconventional gas projects, we put pressure on our government to stop investing in these projects, and we help to inform and mobilise Victorian communities so they can campaign on their own behalf. We focus on being strategic, creative, and as much as possible, fun! The above screen shot is of the Victorian State government’s Mining Licences Near Me site. Go to this link to see what is happening in your area Environment Victoria’s campaign CoalWatch is an interactive resource that tracks the coal industry’s expansion plans and helps builds a movement to stop these polluting developments. CoalWatch provides a way for everyday Victorians to keep track of the coal industry’s ambitious expansion plans. To check what tax-payer money has been pledged to brown coal projects and the coal projects industry is spruiking to our politicians. Here’s another map via EV website (go to their website and you should be able to get better detail from Google Maps: Red areas: Exploration licences (EL). These areas are held by companies to undertake exploration activity. A small bond is held by government in case of any damage. If a company wants to progress the project it needs to obtain a mining licence. Exploration Licence applications are marked with an asterix in the Places Index eg. EL4684*. Yellow areas: Mining Licences (MIN). A mining licence is granted with the expectation that mining will occur. A larger bond is paid to government. Green areas: Exploration licences that have been withdrawn or altered due to community concern. Green outline: Existing mines within Mining Licences. Purple areas: Geological Carbon Storage Exploration areas for carbon capture and storage. On-shore areas have been released by the State Government, while off-shore areas have been released by the Federal Government. The Coal Watch wiki tracks current and future Victorian coal projects, whether they are power stations, coal mines, proposals to export coal or some other inventive way of burning more coal. To get the full picture of coal in Victoria visit our wiki page. Get more info and see the full list of Exploration Licences current at 17 August 2012 here August 2015, Institute for Energy Economics & Financial Analysis – powerpoint: Changing Dynamics in the Global Seaborne Thermal Coal Markets and Stranded Asset Risk. Information from one of the slides follows. To view full presentation go here Economic Implications for Australia 83% of Australian coal mines are foreign owned, hence direct leverage of fossil fuels to the ASX is relatively small at 1-2%. However, for Australia the exposure is high, time is needed for transition and the new industry opportunities are significant: 1. Energy Infrastructure: Australia spends $5-10bn pa on electricity / grid sector, much of it a regulated asset base that all ratepayers fund much of it stranded. BNEF estimate of Australia’s renewable energy infrastructure investment for 2015-2020 was cut 30% from A$20bn post RET. Lost opportunities. 2. Direct employment: The ABS shows a fall of ~20k from the 2012 peak of 70K from coal mining across Australia, and cuts are ongoing. Indirect employment material. 3. Terms of trade: BZE estimates the collapse in the pricing of iron ore, coal and LNG cuts A$100bn pa from Australia’s export revenues by 2030, a halving relative to government budget estimates of 2013/14. Coal was 25% of NSW’s total A$ value of exports in 2013/14 (38% of Qld). Australia will be #1 globally in LNG by 2018. 4. The financial sector: is leveraged to mining and associated rail port infrastructure. WICET 80% financed by banks, mostly Australian. Adani’s Abbot Point Port is foreign owned, but A$1.2bn of Australian sourced debt. Insurance firms and infrastructure funds are leveraged to fossil fuels vs little RE infrastructure assets. BBY! 5. Rehabilitation: $18bn of unfunded coal mining rehabilitation across Australia. 6. Economic growth: curtailed as Australia fails to develop low carbon industries. Analysis: Record surge of clean energy in 2024 halts China’s CO2 rise

In-depth Q&A: Does the world need hydrogen to solve climate change?

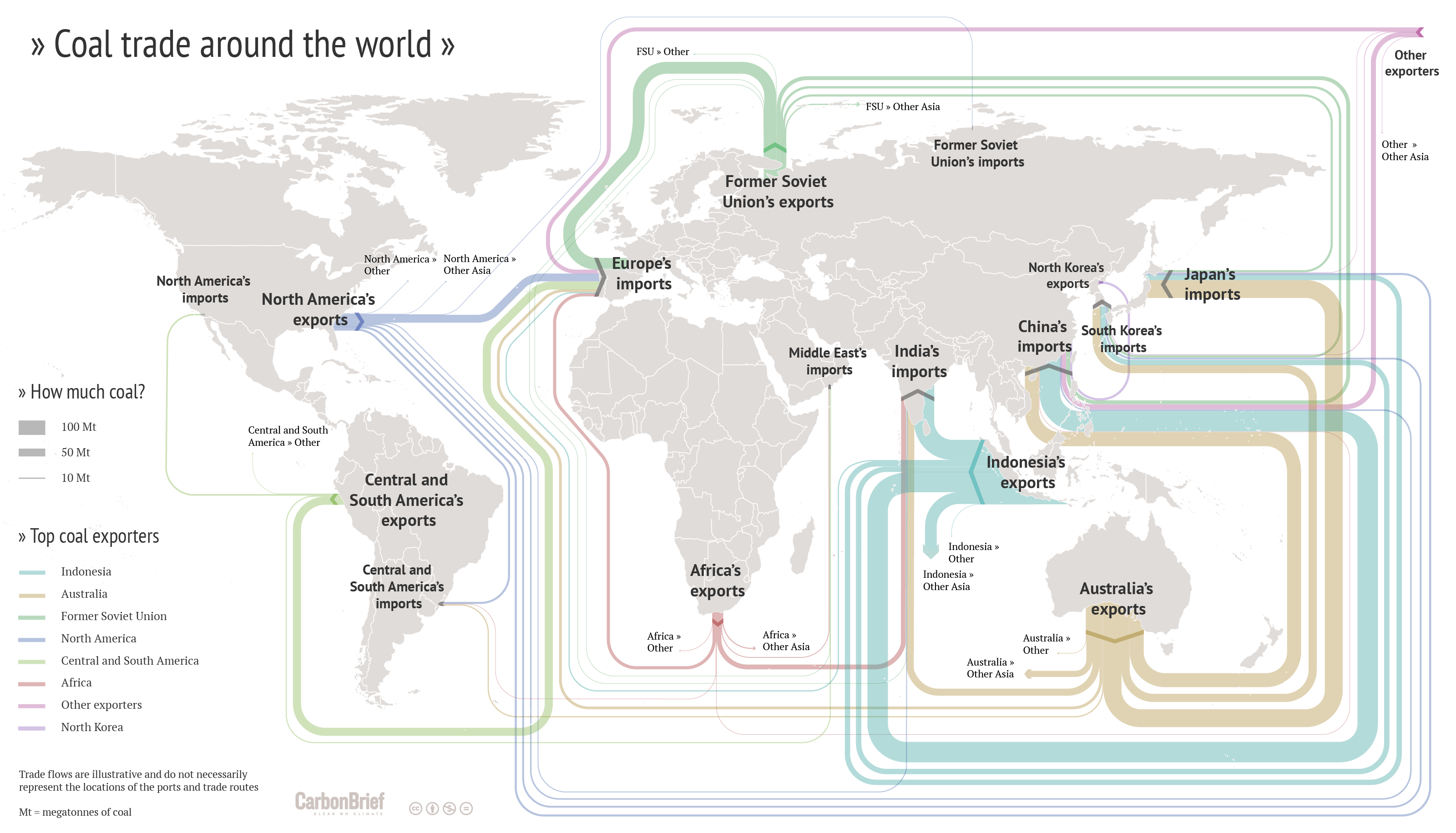

3 May 2016, Carbon Brief, The global coal trade doubled in the decade to 2012 as a coal-fueled boom took hold in Asia. Now, the coal trade seems to have stalled, or even gone into reverse. This change of fortune has devastated the coal mining industry, with Peabody – the world’s largest private coal-mining company – the latest of 50 US firms to file for bankruptcy. It could also be a turning point for the climate, with the continued burning of coal the biggest difference between business-as-usual emissions and avoiding dangerous climate change. Carbon Brief has produced a series of maps and interactive charts to show how the global coal trade is changing. As well as providing a global overview, we focus on a few key countries: Read More here

3 May 2016, Carbon Brief, The global coal trade doubled in the decade to 2012 as a coal-fueled boom took hold in Asia. Now, the coal trade seems to have stalled, or even gone into reverse. This change of fortune has devastated the coal mining industry, with Peabody – the world’s largest private coal-mining company – the latest of 50 US firms to file for bankruptcy. It could also be a turning point for the climate, with the continued burning of coal the biggest difference between business-as-usual emissions and avoiding dangerous climate change. Carbon Brief has produced a series of maps and interactive charts to show how the global coal trade is changing. As well as providing a global overview, we focus on a few key countries: Read More here/cdn0.vox-cdn.com/uploads/chorus_asset/file/3915730/EIA%20coal%20power%20plants.png)

21 April 2015, Climate Council, Will Steffen: Unburnable Carbon: Why we need to leave fossil fuels in the ground.Stern Commission Review

Australia’s Garnaut Review

November 2014 – The Fossil Fuel Bailout: G20 subsidies for oil, gas and coal exploration report: Governments across the G20 countries are estimated to be spending $88 billion every year subsidising exploration for fossil fuels. Their exploration subsidies marry bad economics with potentially disastrous consequences for climate change. In effect, governments are propping up the development of oil, gas and coal reserves that cannot be exploited if the world is to avoid dangerous climate change. This report documents, for the first time, the scale and structure of fossil fuel exploration subsidies in the G20 countries. The evidence points to a publicly financed bailout for carbon-intensive companies, and support for uneconomic investments that could drive the planet far beyond the internationally agreed target of limiting global temperature increases to no more than 2ºC. It finds that, by providing subsidies for fossil fuel exploration, the G20 countries are creating a ‘triple-lose’ scenario. They are directing large volumes of finance into high-carbon assets that cannot be exploited without catastrophic climate effects. They are diverting investment from economic low-carbon alternatives such as solar, wind and hydro-power. And they are undermining the prospects for an ambitious climate deal in 2015. Access full report here For the summary on Australia’s susidisation of it’s fossil fuel industry go to page 51 of the report. The report said that the United States and Australia paid the highest level of national subsidies for exploration in the form of direct spending or tax breaks. Overall, G20 country spending on national subsidies was $23 billion. In Australia, this includes exploration funding for Geoscience Australia and tax deductions for mining and petroleum exploration. The report also classifies the Federal Government’s fuel rebate program for resources companies as a subsidy.

November 2014 – The Fossil Fuel Bailout: G20 subsidies for oil, gas and coal exploration report: Governments across the G20 countries are estimated to be spending $88 billion every year subsidising exploration for fossil fuels. Their exploration subsidies marry bad economics with potentially disastrous consequences for climate change. In effect, governments are propping up the development of oil, gas and coal reserves that cannot be exploited if the world is to avoid dangerous climate change. This report documents, for the first time, the scale and structure of fossil fuel exploration subsidies in the G20 countries. The evidence points to a publicly financed bailout for carbon-intensive companies, and support for uneconomic investments that could drive the planet far beyond the internationally agreed target of limiting global temperature increases to no more than 2ºC. It finds that, by providing subsidies for fossil fuel exploration, the G20 countries are creating a ‘triple-lose’ scenario. They are directing large volumes of finance into high-carbon assets that cannot be exploited without catastrophic climate effects. They are diverting investment from economic low-carbon alternatives such as solar, wind and hydro-power. And they are undermining the prospects for an ambitious climate deal in 2015. Access full report here For the summary on Australia’s susidisation of it’s fossil fuel industry go to page 51 of the report. The report said that the United States and Australia paid the highest level of national subsidies for exploration in the form of direct spending or tax breaks. Overall, G20 country spending on national subsidies was $23 billion. In Australia, this includes exploration funding for Geoscience Australia and tax deductions for mining and petroleum exploration. The report also classifies the Federal Government’s fuel rebate program for resources companies as a subsidy.